The Cheapest Part of a Failed Payment Is the Payment

Ask a finance team what a failed payment costs and the instinctive answer is a processing fee, perhaps a return charge, a few pounds at most. That answer measures the wrong thing. The transaction cost of a failed payroll payment is trivial; the cost of everything it sets in motion is not.

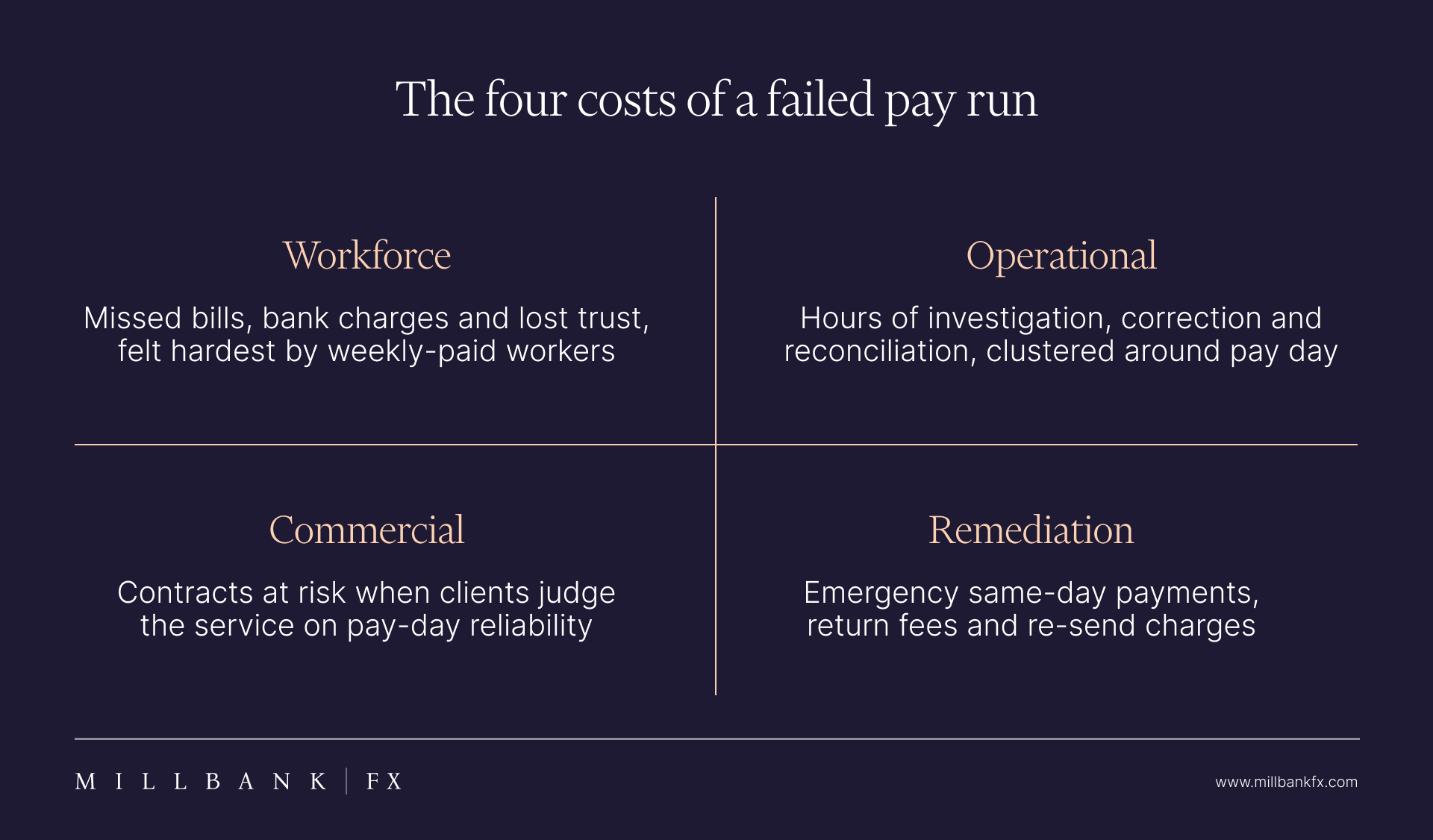

For payroll companies, umbrella companies, and employers running high-volume pay runs, payment failures and late runs generate costs across four distinct areas: workforce impact, operational drag, commercial damage, and remediation expense. Understanding each is the strongest argument for investing in a payment process that prevents failures rather than one that merely reports them.

1. The Workforce Cost: Missed Pay Is Never a Minor Event

For the person on the receiving end, a late salary payment is not an administrative hiccup. Direct debits for rent and bills are timed around pay day; a payment that lands two or three days late can trigger missed payments, bank charges, and real financial stress, particularly for temporary and contract workers on weekly pay who have less buffer to absorb a delay.

The consequences flow back to the business quickly. Workers who are paid late lose confidence in their agency or employer, and in temporary staffing, where workers can often choose between agencies, payment reliability is a genuine retention factor. A reputation for paying accurately and on time is commercially valuable; a reputation for the opposite spreads fast among a contractor community.

2. The Operational Cost: One Failure, Many Hours

Each failed payment sets off a chain of manual work. The recipient contacts the agency; the agency contacts the payroll team; the payroll team investigates the failure, identifies the cause, corrects the detail, and initiates an emergency payment, often through a more expensive urgent channel, and then reconciles the correction against the original run.

Multiply that chain across even a modest failure rate on a large run and the arithmetic becomes uncomfortable. A 1% failure rate on a 2,000-payment weekly run is twenty escalation chains, every week. The staff hours consumed are hours not spent on onboarding new clients or improving processes, and because failures cluster around pay day, they land at precisely the moment the team has least capacity to absorb them.

3. The Commercial Cost: Clients Judge You on Pay Day

For payroll bureaus and umbrella companies, payment execution is the product. A client outsources payroll precisely so that workers are paid correctly and on time; every failed or late payment is a defect in the core service, visible to the client's own workforce.

Repeated failures put contracts at risk in a market where switching providers is straightforward. They also surface in the sales cycle: prospective clients ask about payment reliability, and a provider that cannot evidence a low failure rate is negotiating from weakness. Payment reliability, quantified, is one of the few operational metrics that translates directly into commercial credibility.

4. The Remediation Cost: Paying Twice to Pay Once

Finally, the direct costs. Emergency same-day payments to fix a failure typically cost more than the original payment would have. Failed international payments can incur return fees from intermediary banks and a second set of charges on the re-send. Rejected file submissions on some channels carry their own charges. None of these is individually large; collectively, on a recurring basis, they are a tax on an unreliable process.

Prevention: Where the Failures Actually Come From

Almost all payment failures trace back to a small set of causes, incorrect or outdated beneficiary details, file formatting errors, missed cut-offs, and missing international payment fields, and every one of them is detectable before money moves. Our breakdown of why bulk payment files fail covers the causes in detail, but the structural fix is consistent: validation must happen before release, not after failure.

That means structural checks on account details for every payment in every run, file reconciliation against payroll totals before submission, verified processes for beneficiary changes, and execution routes fast enough that a correction can still land on pay day. Teams can build this discipline internally, or they can use a provider whose service includes it, the trade-offs are set out in our guide to choosing a mass payment provider.

How Millbank FX Keeps Failure Rates Low

Millbank FX operates a fully managed mass payment service in which every file is cleaned and validated by our team before payments are released. Issues are resolved with you before money moves, most payments are processed same-day, and where a payment is returned by a receiving bank you are notified immediately with the specific reason.

The outcome is the metric that matters: across all mass payment processing, we have maintained a 0.05% kickback rate. We are authorised by the FCA, client funds are safeguarded, and we support payments in over 80 currencies to 120+ countries.

If you want to quantify what payment failures are currently costing your business, book a 15-minute demo. Bring your failure numbers, and we will show you what a pre-validated run looks like on your own file.