The Question Behind Every Provider Conversation

When a business considers moving its payment processing away from a bank, one question sits underneath every other consideration: what happens to our money while it is with the provider? A weekly pay run can mean transferring six or seven figures to a firm that is not a bank, and finance teams are right to want a clear, factual answer before doing so.

The answer rests on two concepts that are frequently mentioned in provider marketing but rarely explained properly: FCA authorisation and safeguarding. This article sets out what each one means in practice, what it does and does not cover, and how to verify a provider's status for yourself.

What FCA Authorisation Means for a Payment Institution

In the UK, firms that provide payment services, executing transfers, operating payment accounts, providing money remittance, must generally be authorised or registered by the Financial Conduct Authority under the Payment Services Regulations 2017. An authorised payment institution has been assessed by the FCA against requirements covering, among other things, its capital, its governance and controls, the fitness of the people running it, and its arrangements for protecting customer funds.

Authorisation is an ongoing status, not a one-off stamp. Authorised firms report to the FCA and remain subject to its supervision and rules. It is important to be precise about what this means: authorisation confirms that a firm has met and continues to be held to regulatory standards. It is not an endorsement of the firm by the regulator, and it is not a guarantee of commercial outcomes. Any provider presenting FCA authorisation as either of those things should be treated with caution, credible firms state their regulatory status as a fact and explain it accurately.

What Safeguarding Means, in Plain Terms

Safeguarding is the specific mechanism that protects client money held by an authorised payment institution. The core requirement is separation: relevant funds received from clients must be held separately from the firm's own money, typically in designated safeguarding accounts with a credit institution, rather than mixed with the firm's operating capital.

The purpose of this separation is straightforward. Money you send to the provider for payment processing is not the firm's money to use in running its business. It is held apart, so that client funds are identifiable and protected as client funds. In the event a firm fails, the safeguarding regime is designed so that safeguarded client funds are returned to clients, with those claims ranking ahead of the firm's ordinary creditors in respect of the safeguarded pool.

Safeguarding is a different mechanism from the deposit protection that applies to bank deposits. It works through separation of funds rather than through a compensation scheme, which is why authorised payment institutions describe client money as safeguarded rather than using bank-deposit terminology. The practical takeaway for a finance team is to confirm that a provider safeguards relevant funds and can explain its arrangements clearly.

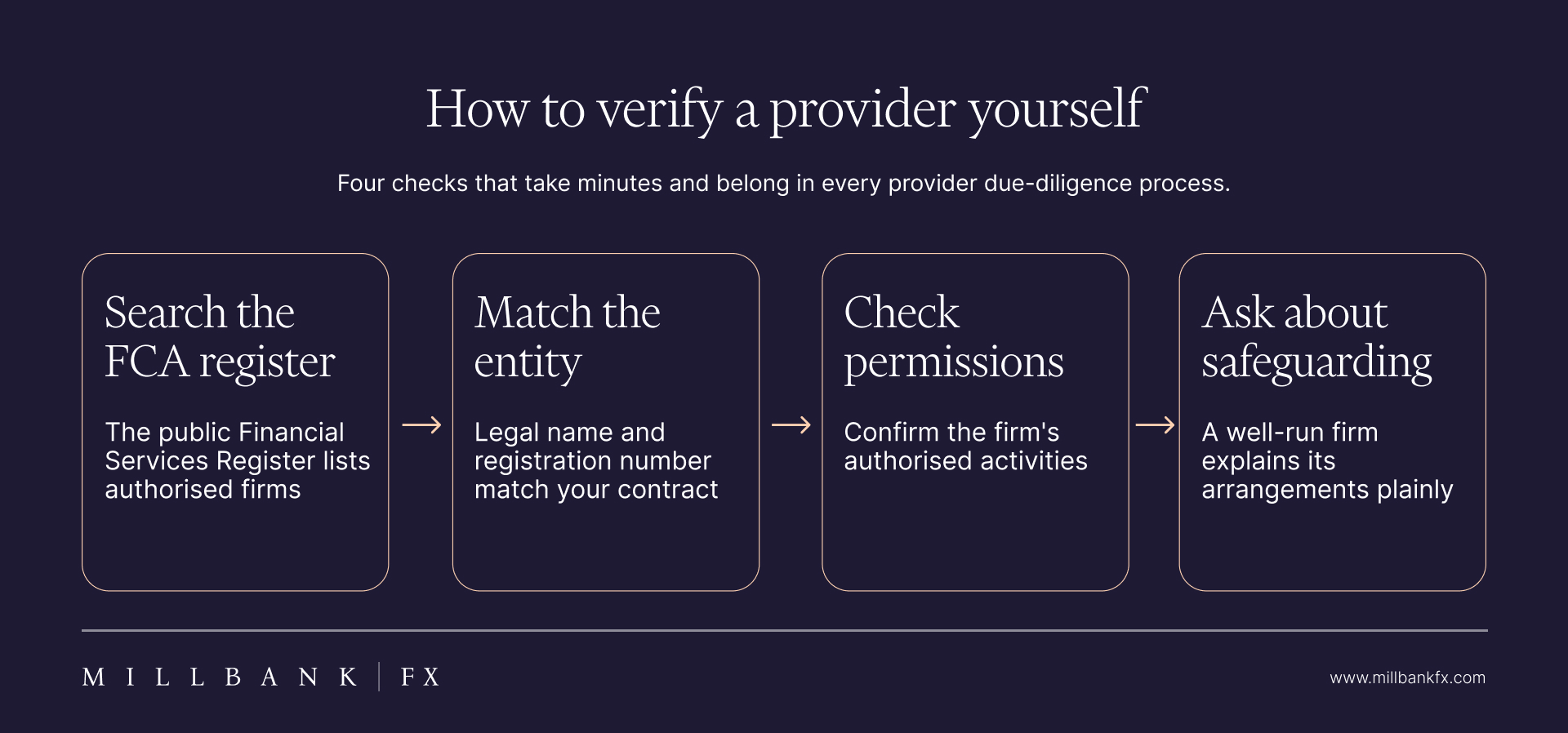

How to Verify a Provider's Status Yourself

Verification takes minutes and should be standard due diligence before onboarding any payment provider. Search the firm on the FCA's public Financial Services Register, which shows whether it is authorised or registered, under which regime, and with what permissions. Check that the legal entity name and registration number on the register match the entity named in your contract, group structures can include multiple entities with different statuses. Then ask the provider directly how client funds are safeguarded and where safeguarding accounts are held; a well-run firm will answer plainly.

Beyond regulatory status, it is reasonable to ask about the operational controls that sit around your money: how payment instructions are authenticated, what dual-control or verification steps apply to outgoing payments, and how the provider ensures funds are only paid out on instructions from the client. These controls, alongside safeguarding, are what determine day-to-day security in practice. Our mass payment provider checklist places these questions within a broader evaluation framework.

Why This Matters Specifically for Mass Payments

Mass payments concentrate the question. A business making occasional transfers holds funds with a provider briefly and in modest amounts. A payroll company or umbrella business funding weekly runs may routinely place large sums with its provider ahead of each cycle. The larger and more frequent those balances, the more the provider's regulatory status, safeguarding arrangements, and payout controls matter, and the more they belong in your provider selection criteria alongside speed, validation, and cost.

How Millbank FX Holds and Protects Client Funds

Millbank FX is authorised by the Financial Conduct Authority as a payment institution (Reg. 787366). Client funds are safeguarded: they are held in safeguarded accounts, kept separate from the company's operating funds, and are only paid out on instructions taken from the client. Outgoing payments in our managed mass payment service are subject to a dual-check process before release.

We have processed over £6 billion in payments since 2016 for payroll companies, umbrella companies, recruitment firms, and high-volume employers, and clients have direct access to the team processing their payments throughout every run.

If you are conducting due diligence on payment providers, we are happy to walk through our regulatory status, safeguarding arrangements, and payment controls in detail. Book a 15-minute call and bring your questions.